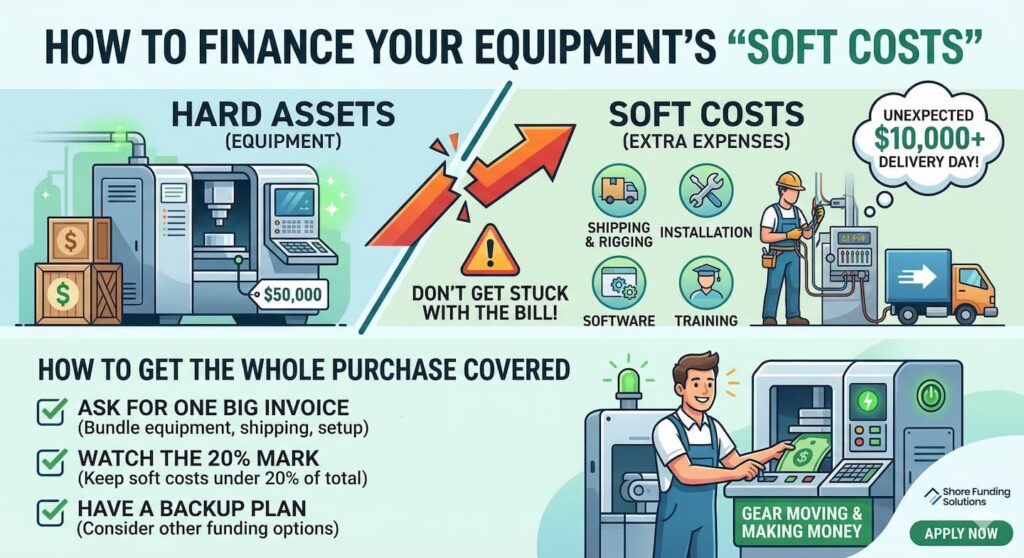

Buying new equipment can be a major move in the right direction for your business, but there is a hidden trap that catches a lot of smart business owners off guard. You find the perfect machine, you then get a quote for $50,000, and find an approval for exactly that amount through equipment financing options. Then the machine shows up at your door, and you learn you still have to pay for the shipping, the electrical setup, and the specialist to install it .

In our industry, we call these extra fees “soft costs.”

While the machine is the main thing you’re purchasing, these extra expenses are what actually make the purchase more than you might have planned for. If you don’t plan for them ahead of time, you might end up writing a personal check for an additional $10,000 on delivery day just to get the power turned on.

Why Most Lenders Focus on “The Iron”

Think of it from the lender’s side. They like “hard assets” like the things they can see and touch, like a truck or a forklift. If things go south, they can take the machine back. But they can’t repossess “labor” or “shipping.” Once that money is spent on an electrician or a delivery driver, it’s gone.

Because of that, many no documentation loan programs have a limit on how much of these costs they will cover. Common ones to watch out for are:

- Shipping and Rigging: Getting heavy gear from the warehouse to your shop floor.

- Installation: Professional wiring, plumbing, or bolting things down.

- Software: The digital “brain” that makes the hardware actually work.

- Training: Paying an expert to show your crew how to use the new tools.

How to Get the Whole Purchase of Your Equipment Covered

The trick is to show the lender the “total cost” instead of just the sticker price. Here is how you can set yourself up for a better result:

- Ask for One Big Invoice: Talk to your vendor. Ask if they can bundle the machine, the shipping, and the setup into one single total. When a lender sees an invoice for “Equipment and Installation,” they are much more likely to approve the whole thing.

- Watch the 20% Mark: Most lenders are okay with soft costs as long as they stay under 20% of the total loan. If you keep it in that range, you probably won’t have to use your own cash.

- Have a Backup Plan: If the equipment loan has a strict limit and you’re still short, you can look into business loans with no credit check to help with those final setup fees. It’s better than draining your personal savings.

Here is an infographic to explain soft costs and what you should look for.

Let’s Get Your Gear Moving

At Shore Funding Solutions, we want to see that equipment actually working for you, not sitting in a crate because the installation wasn’t covered. We know that a machine is only an asset once it’s making you money.

Finally, don’t just look at the price tag on the machine. Think about what it takes to get it plugged in and running. If you’re ready to see what your options look like, let’s get started applying now .