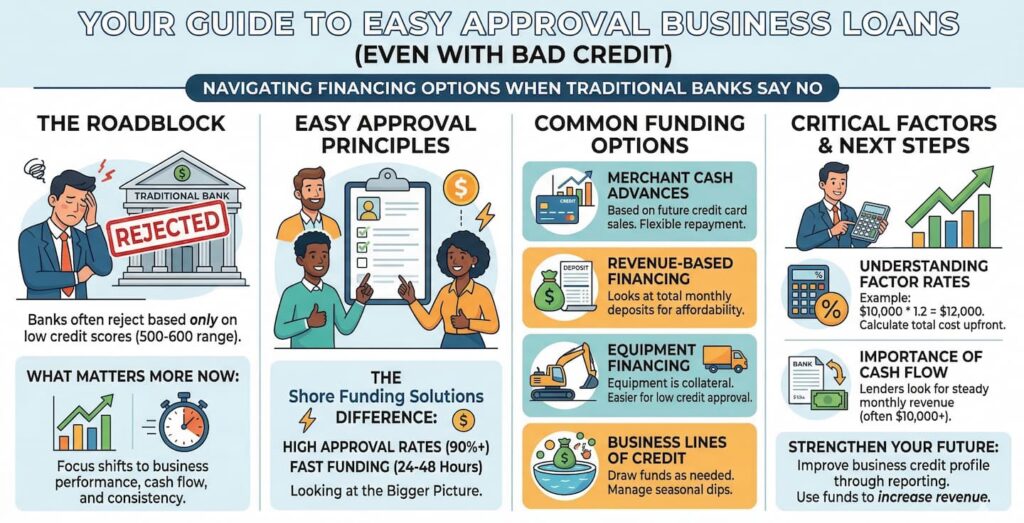

If you are a business owner navigating the world of financing with a less than perfect credit score, you likely know how stressful the process can feel. Traditional banks often focus heavily on your personal credit history, which can lead to immediate rejections. However, there is a different path forward. Many modern lenders now prioritize the health of your business and your consistent cash flow over a single number on a credit report. This guide will help you find the right funding to strengthen your operations.

The Reality of Easy Approval Loans

When people speak about easy approval, they are usually referring to a speedier and more flexible process. At Shore Funding Solutions, the focus remains on your business performance rather than just your past financial hurdles. By looking at your revenue and time in business, lenders can offer approvals that seem out of reach at a standard bank.

High Approval Rates and Fast Funding

Alternative financing providers often boast high approval rates. For instance, Shore Funding Solutions maintains a 90% approval rate by looking at the bigger picture of your company. You can often see funds in your account within 24 to 48 hours. This speed is vital when you need to cover a sudden expense or take advantage of a fleeting opportunity.

Common Funding Options for Bad Credit

If your credit score is in the 500 to 600 range, you still have several paths to explore. Each option has different requirements and benefits based on how your business operates.

- Merchant Cash Advances: These are based on your future credit card sales. The lender provides a lump sum and you pay it back through a percentage of your daily sales.

- Revenue Based Financing: Similar to an advance, this looks at your total monthly deposits to determine how much you can afford to borrow.

- Equipment Financing: If you need a specific piece of machinery or a vehicle, the equipment itself serves as collateral. This reduces the risk for the lender and makes it easier to get an approval despite bad credit.

- Business Lines of Credit: This gives you a pool of funds to draw from as needed. You only pay for what you use, which is excellent for managing seasonal dips.

Critical Factors to Consider Before You Apply

Before you start your application, it is important to understand the costs involved. While these loans are easier to get, they often come with different structures than a typical mortgage or car loan.

Understanding Factor Rates

Instead of a standard interest rate, many bad credit loans use a factor rate. If you receive $10,000 with a factor rate of 1.2, you will owe $12,000 in total. It is important to calculate this total cost upfront so you can ensure the return on your investment justifies the expense.

The Importance of Cash Flow

Lenders will often ask for your last three to six months of bank statements. They want to see that you have a steady stream of income. Most providers look for at least $10,000 in monthly revenue to confirm that your business can comfortably handle the repayment schedule.

How to Improve Your Chances for Future Loans

Taking a loan now is not just about getting immediate cash. It is also an opportunity to build a better financial future for your company.

Verify Credit Reporting

Ask your lender if they report your payments to business credit bureaus. By making on-time payments, you can actually improve your business credit profile. This will help you qualify for lower rates and larger amounts in the future.

Use the Funds to Increase Revenue

The best way to use high-cost capital is to put it toward something that generates more money. Whether you are buying inventory in bulk or launching a marketing campaign, using the funds to grow your sales will make the loan much easier to pay back.

Why Shore Funding Solutions is a Strong Partner

Since 2014, Shore Funding Solutions has been helping small businesses across the country find customized financial answers. Based in Melville, NY, this team understands that a credit score does not tell the whole story of your hard work.

With a simple seven question application and a commitment to five star support, Shore Funding Solutions acts as a bridge to the capital you need. You can find out what you qualify for without the long wait times or the rigid requirements of a traditional institution.

Can I get a business loan even if I have a lousy credit history?

Yeah, it’s definitely doable. There are loads of alternative lenders who focus more on the financial health of your business, rather than just your personal credit score. Think merchant cash advances, revenue based financing, equipment financing, and business lines of credit – these options can be up for grabs even if your credit’s sitting in the 500 to 600 range.

Here is an infographic to help you understand options.

What’s the easiest business loan to get approved for when you’ve got bad credit?

Typically it’s merchant cash advances, revenue based financing and equipment financing. That’s because these options are more interested in your business’s revenue, future sales or the value of any collateral you’ve got rather than what your credit score looks like. That makes it a lot more likely they’ll say yes.

How long does it take to get my hands on the cash after putting in a business loan application with bad credit?

Loads of alternative lenders can get funding out to you within 24 hours to 48 hours after they’ve given you the thumbs up. That’s perfect for covering unexpected bills or nipping into a new business opportunity.

What do lenders actually look at when they’re deciding whether to lend you cash for your business, despite your bad credit?

They tend to care more about your business’s revenue, how long you’ve been in business and how much cash you’re bringing in each month rather than what your personal credit score is. Most of the time they’ll want to see at least 3- 6 months of bank statements to make sure your business is in a solid position to pay them back.

How can I increase my chances of getting approved for one of these business loans with bad credit?

The best bet is to make sure you’re bringing in consistent cash, the revenue for your business is strong and you choose a financing option that actually works for you. Plus, asking lenders how they handle payments to business credit bureaus and making sure you pay on time will help improve your business credit profile so you’re in a better position for future loans.

Finding a business loan with bad credit is entirely possible when you know where to look. By focusing on your revenue and choosing the right type of financing, you can get the capital necessary to move your business forward.